Complexity is a tax

Complexity is a tax

Life, death, thermodynamics and the certainty that complexity is rarely worth it

On the wittier end of life’s certainties we have death and taxes. On the more rigorous end we have the laws of thermodynamics the second of which is: that disorder in a system will increase over time if left unchecked (entropy).

It is those checks and balances - an increase in control and complexity - which shield us from the worst of entropy. Yet if we deploy complexity too enthusiastically in an effort to control the system: businesses calcify and competitiveness decreases.

For us, success is easier to come by when owners, managers and businesses have a keen eye on the trade off between the potential benefits of greater control and the risks that come hand-in-hand with greater complexity.

What might “bad complexity” look like?

Here are some examples:

Employees’ diaries full of internal meetings

Reporting taking up large proportions of managerial and non-managerial staff time

“Best practice” framework implementation where usage generates an administrative burden for which a company may not have appropriate scale

Multiple business lines taking focus (and performance) away from the core: a management overhead for managers and line staff alike

Points of breakage or delay with managers in positions of ‘control’

Those signs generate symptoms:

Employees burning out through context switching

Poor performance relative to your peer group over the medium+ term

High levels of unwanted employee turnover

Increasing complexity in a system - increasing the level of control - requires time. That time has to be taken away from other activities: product development, talking to customers, etc. Time is exceptionally valuable so we should be prepared to safeguard it or, at least, be appropriately circumspect when introducing more of it. Clearly as businesses evolve and grow they need evolved and/or new rails to direct activity. However in our experience it is common to see a poor trade-off where complexity is throttling activity rather than enabling it.

Complexity is an overhead, a tax, with quantifiable and more subtle effects, be wary of its introduction. Occam knows best.

↑ control = ↑ complexity = ↑ time required

We have been reminded of our dislike of complexity twice recently: once in a deal that we were close to (analysis + model further below) and in a conversation with an investor who has successfully created one of the UK’s most successful HoldCo conglomerates. Over coffee they talked about their approach as the majority owner of 40 companies: “We’re lazy investors, by design.”

Clearly this wasn’t referring to wanting an easy life, rather, letting the management teams of their portfolio businesses get on with things. As an investor, they have a very lean operation and want to keep it that way. There’s a perfectly good assumption at the core of the operational model: let the experts get on with their own businesses, be there when you can add value and be relevant.

They’re clearly on the less complex end of things and so expose themselves to the risks of entropy: what happens if founders/owners check out after you’ve allowed them to realise some of their wealth tied up in the company? How can you get to a level of trust over the management information and reporting that you receive? How will business owners react to having a new majority owner (who isn’t heavily involved)? Can people be trusted to stick to the plan? (We’ll return to this larger topic of approaches to people management in an issue in the near future.)

They’ve made a choice as an organisation: have fewer people, own more economics, choose management teams well, understand strength of cashflow in-and-out…and everything should be ~ok.

We came close to investing in an internet advertising business in recent months. We didn’t end up investing for a number of reasons however there were a couple of things which had us excited about the deal: (1) an extraordinary amount of complexity within the company, (2) a superficially good price.

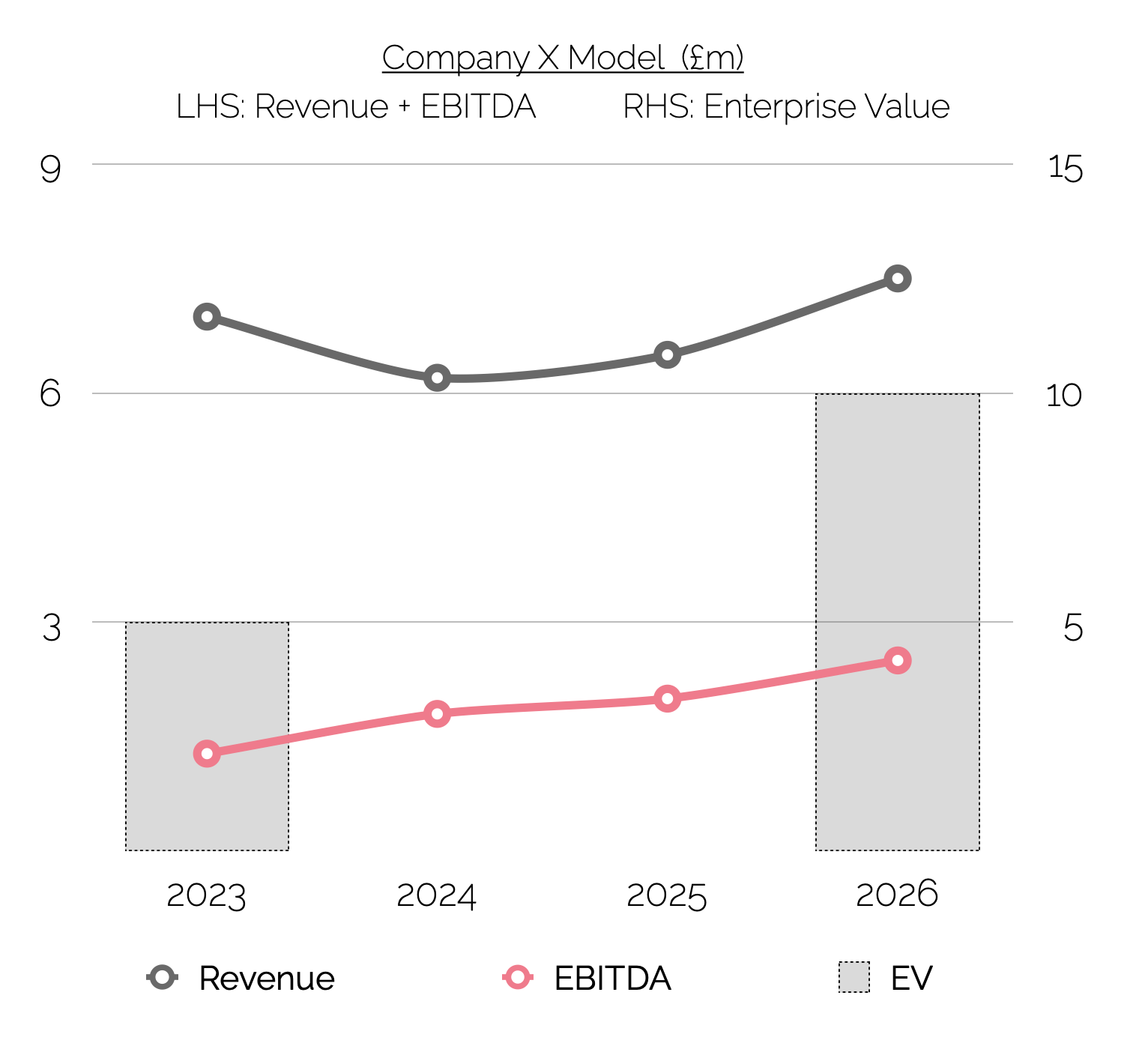

For regular readers and our investors you’ll know that we like to see some ‘fruit on the tree’. The fruit being areas that can be boosted, changed for the better, or streamlined. We’re a long, long way from a PE chop-shop however it is remarkable how many opportunities that we see with clear opportunities to simplify businesses. In this case our model looked as below.

Revenues to scale modestly from £7 to £7.5m over 3 years with a year_1 retrenchment, EBITDA profitability from £1.3m to £2.5m. Assuming the same purchase and exit multiple for conservatism it is a case that offers 26% IRR. Our plan as we discussed it with management was simple: focus on the core. This was driven by a two key interventions:

Shutter two minor business lines which were, charitably, at prototype stage. Someway from monetisation and with different business models to the lead gen core.

Rationalise lead nurturing. While a significant revenue contributor of ~£700k (~10%), unprofitable + a horrible cash cycle (working capital intensive).

Neither of these interventions would be particularly high risk and relatively quick and easy to execute. The anticipated result of this push for lower complexity: higher levels of profitability (the business is more valuable). However there would have been a neat side effect: we would have stripped away the management overhead associated with this complexity, freeing up time. Precious, time.

Tikto

At Tikto, we purchase majority stakes in EBITDA profitable businesses and follow that up with incremental growth capital. We bring our network of experienced operators to help execute a business plan for the next phase of our portfolio companies’ growth.

Get in touch: hello@tiktocapital.com

NB// if you’ve had experiences of either good or bad complexity in your experience, we’d love to hear from you.