Shoulder season and blog performance

Shoulder season and blog performance

Zero 2023 predictions included within

Like us, we are sure that you’ve noticed no shortage of predictions in your inboxes. Rather than provide you with more of the same we’ve spent shoulder season considering the performance of our blogging efforts since we started writing in July. It’s a bit of fun but digging into the numbers reveals some observations that may be useful for us all as we move into the New Year.

Why blog at all?

Assessing performance is easier in the context of “the goal”. So, why do we write at all? Two reasons.

We like writing. It helps us to embed learnings and we like to share those learnings.

Network nurturing. We want to remind our network - those that send us deals, work on transactions with us, investors, etc. - that we exist.

Insofar as #1 goes: mission complete. We began writing in July and we’re still at it, still enjoying it.

Has blogging helped us nurture our network?

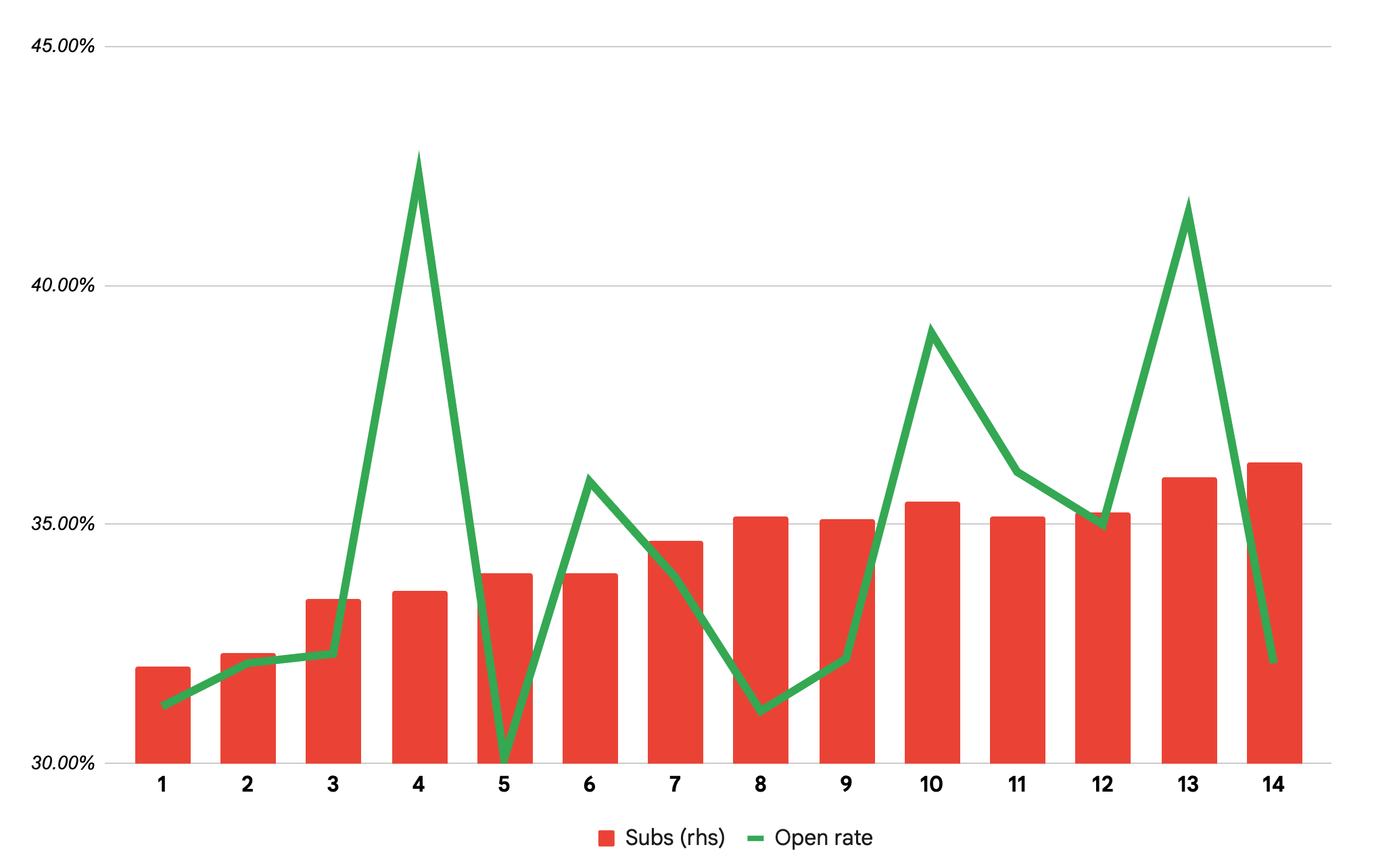

This is where the stats start to come in, and where we start to get more questions than answers as we look into the detail. Across the 14 issues that we’ve written to-date here’s what our open rates look like (left hand axis) and our subscriber count (right hand axis).

A very simple answer to the question as to whether the blog is performing well is to compare our average open rate with industry comparators. Market standard “Professional Services” email campaigns achieve an average 21.9% open rate whereas we’ve achieved 34.6%. On that basis we are doing well and it would seem like a worthwhile “channel” to stick with.

Next up, the learnings and whether or not we’ve been improving over time.

What’s gone well, what’s gone less well

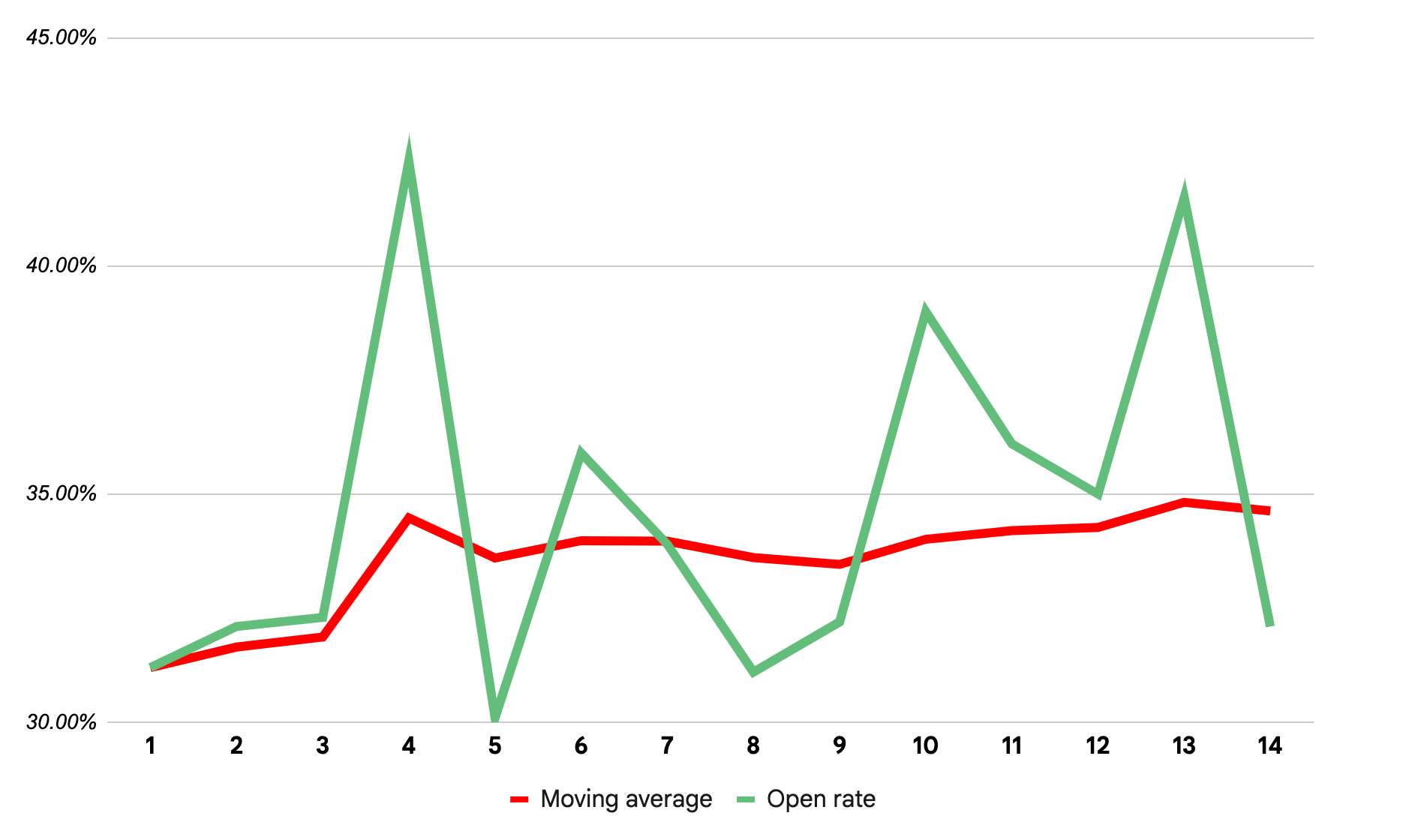

Looking at some more continuous analysis helps us to understand whether we are going in the right direction.

Here’s that same open rate data, though this time with a moving average plotted too.

We’re raised the average open rate from 31.2% to 34.6% over the course of the half-year. We also have 74% more subscribers than we had when we began. Both positive results.

However, we can see that there are some considerable swings in performance from issue-to-issue. What drives that, and how can we optimise our content for the year ahead? There aren’t enough data points here to do any real statistics but there are some messages that come through from observing the data:

When the title has been a question (replete with question mark) we’ve achieved >40% open rates: Where did all the growth go? and Whatever happened to digital transition?

Oddly, there’s actually a weak negative correlation between length of blog and open rates. That said, none of our issues are particularly long and we almost always manage to keep it to a 5 minute read (1000 words) or less with Red flags: employee churn being the only exception at 1383 words

Subject-wise, issues which clearly contain “advice inside” look to perform the best on-average though the highs-and-lows have all been “market commentary and analysis”. From a sample size of 1 “ESG” seems popular with ESG, the UN and investing at the early stage coming in with a bronze-medal open rate of 39.0%

The day that we publish seems to have little effect on open rates

It’s not clear that writing more regularly affects performance (which is good because our promise to you is to only hit your mailbox when we have something interesting to say + we have the time to write…which isn’t every week)

What’s next

We’ll continue roughly as is. There might be some more titles posed as questions (not doing a good job of that so far) though we don’t want to be click-bait-y or thirst-trap-y. We’ll continue keeping the issues short and sweet. We’ll look to write more issues conspicuously containing “advice inside” and look to expand the Red Flags series. We’ll also write more content which covers the intersection of ESG and the world of SMEs.

We’ve also re-platformed and this is the first issue that you’ll receive from our new home at Substack. We liked Revue for the nifty Twitter native feature but when Elon took the reins it was only a matter of time before non-core became non-existent. So it is the case with Revue. Substack prides itself on helping blogs gain more subscribers through their “goodwill growth loop” so here’s hoping that our new home will work out well.

Tikto

At Tikto, we purchase majority stakes in EBITDA profitable businesses and follow that up with incremental growth capital. We bring our network of experienced operators to help execute a business plan for the next phase of our portfolio companies’ growth.

Get in touch: hello@tiktocapital.com

We hope that you’ve had a great holiday season. For now, happy Friday, Happy New Year, and we’ll see you on the other side.